A beginner’s guide to getting a car loan in NZ

Buying a new car is exciting, but it can also be intimidating – particularly if it’s going to be one of the most expensive assets you’ve ever bought.

Many people may be reaching the point in life where they’re ready to upgrade their old ride to a newer, safer or more reliable car, but they don’t have enough savings put aside to drop $20,000+ in one go.

In these scenarios, buying a car on finance is one of the common routes people take. Unfortunately for first timers, the process can seem complicated and leave people apprehensive or confused.

Marac has been helping Kiwis get on the road for more than 65 years, so we’re well-versed in the vehicle finance process. As such, we figured we’d put together a guide to shed some light on how getting a car loan actually works.

Want to read this in a more visual format? Click here to jump down to the infographic.

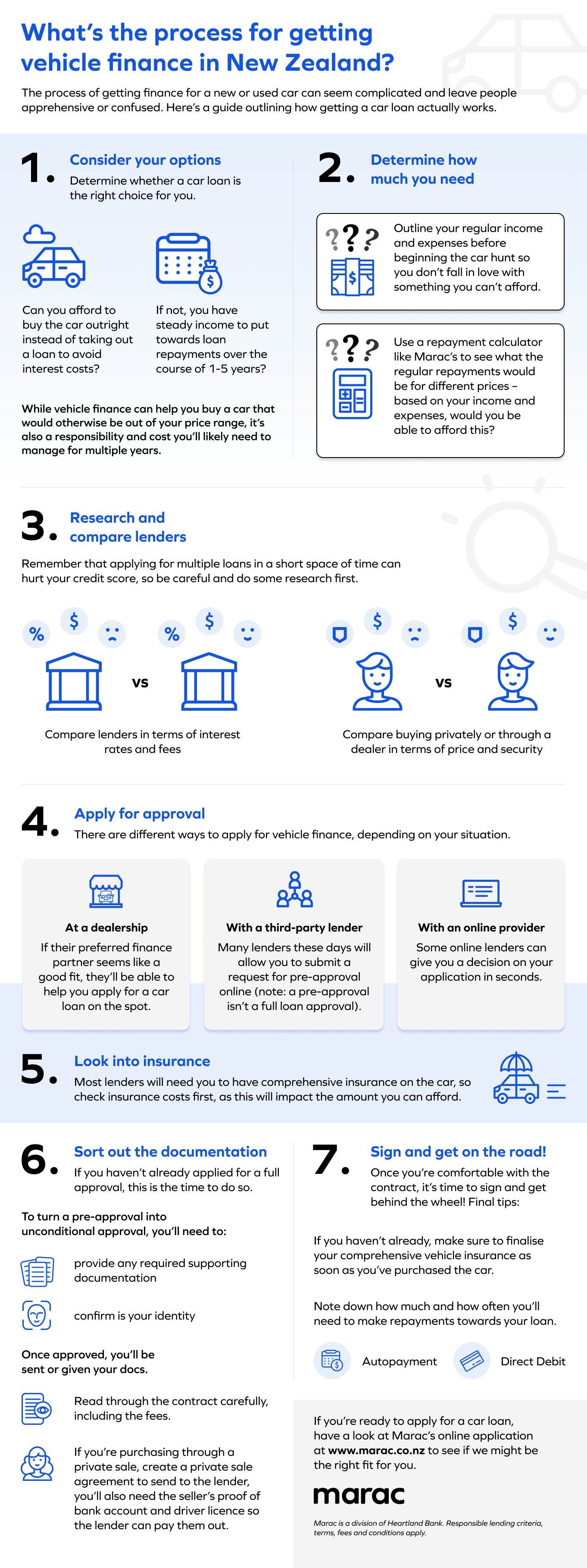

What’s the process for getting vehicle finance in New Zealand?

1. Consider your options

To begin with, you’ll need to determine whether a car loan is the right choice for you. Can you afford to buy the car outright instead of taking out a loan? For many people, the answer to this is no – in that case, do you have steady income to put towards regular loan repayments over the course of 1-5 years?

It’s important to recognise that while vehicle finance can help you buy a car that would otherwise be out of your price range, it’s also a responsibility and cost you’ll need to manage over the next few years. Doing some consideration up front can help you determine whether it’s the right option for you.

2. Determine how much you need

If you haven’t started looking at cars, it’s a good idea to outline your finances – otherwise you might end up falling in love with a car you can’t afford. Your regular income and expenses will play a large role in determining how expensive a car you’ll be able to get.

One way to get a sense for how much you can afford is by using a repayment calculator, like the one on the Marac website. Plug in a realistic amount you think you would spend on a car and see what the regular repayments would be – based on your income and expenses, would you be able to afford this?

If so, great! You’re now ready to figure out which finance provider might be best for you.

3. Research and compare lenders

When you’re looking for a car loan (particularly if you’re in a rush), it can be tempting to send applications in to various lenders that “don’t look dodgy” in the hopes that something will stick. However, applying for multiple loans in a short space of time can have an unwelcome effect on your credit score, so be careful.

Instead, do some digging into your options before applying. Compare both interest rates and fees – some lenders might have lower interest rates but charge exorbitant amounts for establishment, early repayments, refinancing, or discharging the vehicle.

Another thing to consider will be whether you’re buying privately or through a dealer. Buying a vehicle through a dealer might come at a somewhat higher price, but it’s often a more secure option than buying privately, as you may be able to return the vehicle if it’s faulty.

*A side note: if you’re buying privately, we highly recommend getting a pre-purchase inspection to make sure you know exactly what you’re buying!

When buying through a dealer, keep in mind they may have a preferred finance partner, and applying through the dealership will mean the dealer can help you through the process on the spot. With that said, do make sure to research and compare the finance partner’s rates, reputation and fees with others to make sure you’re choosing the lender that’s right for you.

4. Apply for approval

If you’ve found a car at a dealership and their preferred finance partner seems like a good fit, the process is straightforward – they’ll be able to help you apply for a car loan then and there.

If you don’t yet have a car in mind or you’re interested in applying directly with a finance provider, many lenders these days will allow you to submit a request for pre-approval online. Keep in mind that for many lenders, a pre-approval isn’t the same as a full loan approval.

Some providers, like Marac, offer online applications that can give you a decision on your application in minutes, subject to lending criteria – this is great if you’re looking for a quicker process to fit into your busy schedule, with fewer person-to-person touchpoints. In certain cases, you could be given a full approval on the spot, and in many other cases, all you need to provide to become fully approved is your proof of income.

Once you’ve got your approval or pre-approval, you can (if you haven’t already) jump headfirst into the hunt for your new car.

5. Look into insurance

Found a car you like? Next step is to check how much insurance would cost, as this will impact the amount you can afford (depending on how expensive the car is to insure). Most lenders will need you to have comprehensive insurance on the car, so this is an important expense to understand before committing to the purchase.

Now is also a good time to consider whether there are any other insurance products you would like to purchase, like mechanical breakdown insurance, payment protection insurance, or guaranteed asset protection. It’s definitely worth asking your dealer or lender about the pricing and benefits of these products to see if they suit your needs and budget.

6. Sort out the documentation

So you’ve found the vehicle you’d like to buy – if you haven’t already applied for a full approval, this is the time to do so. If you previously got pre-approved for a loan, you may also need to provide supporting documentation to the lender in order for them to convert it into an unconditional approval.

One of the things your finance provider will need to confirm is your identity, which can be done either by you scanning in a certified copy of your driver’s license, or through facial recognition. This kind of biometric technology can help speed up the process by reducing the back and forth, so check to see if your lender offers it.

Once approved, you’ll be sent some documentation – or handed it on the spot, if you’re applying through a dealership. Make sure you read through the contract carefully, including checking out the fees (though these can change over time), to make sure you understand what you’re signing up for.

If you’re purchasing through a private sale, you’ll want to create a private sale agreement (there are templates online) to send to the lender, plus the seller’s proof of bank account and driver licence so they can be paid by the lender.

7. Sign and get on the road!

Once you’re comfortable with the contract, it’s time to sign and get behind the wheel! Some lenders offer online signing capabilities, meaning you don’t need to print, sign and scan your documentation – this can also save a lot of time. If you haven’t already, make sure to follow through with setting up your comprehensive vehicle insurance as soon as you’ve purchased the car. That way you’ll be protected from the moment you drive it away.

Your finance provider will let you know how much and how often you’ll need to make repayments towards your loan. You can either set this up as an autopayment or they can Direct Debit your account.

There are many different paths a person can take when buying a car, depending on whether you’re buying privately or through a dealer, finding a car first or getting pre-approval first. This means the process will look different for everyone, but hopefully our guide provides a good indication of the things that are important to consider and account for when taking out a car loan.

For more information about car loans, check out the Marac blog or some of the common questions people ask about our vehicle finance. And if you’re ready to apply for a car loan, have a look at our online application to see if we might be the right fit for you.

Responsible lending criteria, terms, fees and conditions apply. Marac is a division of Heartland Bank.